We'd like to thank Mark Daoust, owner of Quiet Light Brokerage, for giving us permission to reprint his blog post on SBA loans, part 1 of which is below. Mark is the go-to-guy for the purchase or sale of online eCommerce businesses and if you have an interest in that space, we encourage you to contact him at inquiries@quietlightbrokerage.com.

The US Government's Small Business Administration lends up to $5 million that businesses that meet certain criteria. The post below talks about the general requriements of an SBA loan while part 2 will get into the process of applying for an SBA loan.

More information about the SBA process can be found on the SBA's website here.

Cheval Capital, Inc.

Disclaimer: This post is for general information purposes and is not meant to be taken as financial advice, a recommendation to buy or sell any stocks mentioned above, a comprehensive discussion of valuation or how to do the calculations discussed. Please be sure to consult your financial advisors when valuing your company, considering the sale of your business or making other financial decisions.

------

How To Buy An Online Business With An SBA Loan - The Requirements

I used to hate it when a buyer suggested using an SBA loan to acquire one of my client’s businesses. But it is an option more and more buyers are opting to use.

During the Great Recession of 2009, SBA-backed loans were extremely difficult to get as the entire lending industry re-evaluated how loans were being written. But today, SBA lending is alive and robust.

My opinion used to be that SBA loans were slow and uncertain. They seemed to be the choice of buyers who really had no other choice. But I was wrong, and I am happy to admit that! SBA loans can be a great option for both buyers and sellers of Internet-based businesses.

So what is involved when applying for an SBA loan? How do you qualify? What does the process look like? I reached out to one of our recommended lenders at a major bank to ask him every question I could think of about SBA loans, as well as relying on our extensive experience at Quiet Light Brokerage.

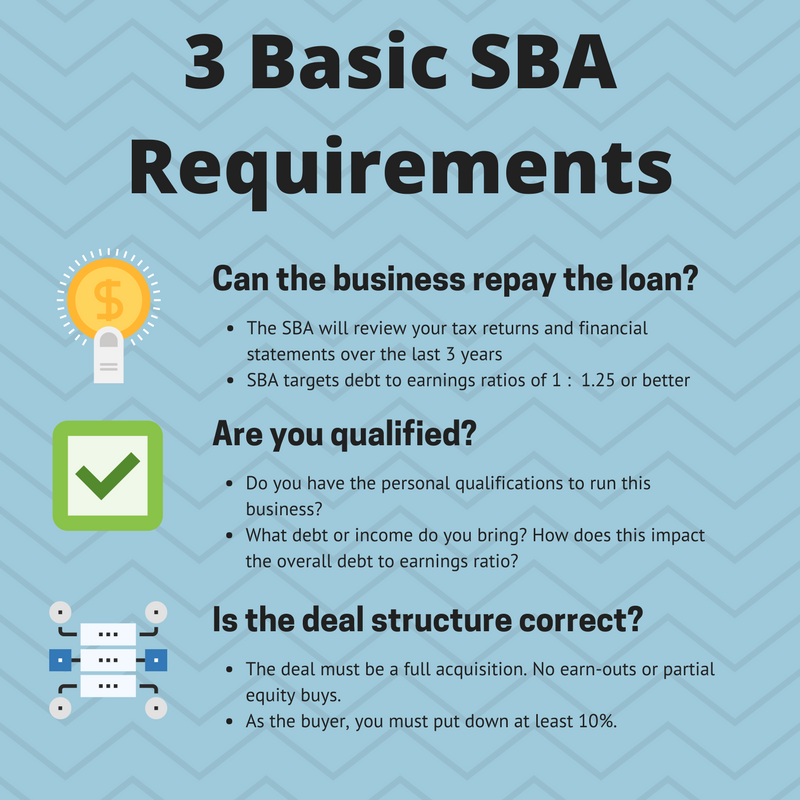

The Three Basic Requirements For an SBA Loan

There are a lot of individual boxes your bank and the SBA will require you to check before getting an SBA loan. But at the broadest level, an SBA loan has just three basic requirements.

First, is the business being acquired able to sufficiently service the loan? In other words, will you be generating enough revenue to pay back the SBA?

Second, the bank will look at you, your personal financial situation, and your qualifications. Even if the business can service the loan, the bank will want to make sure it can do this under your ownership.

Finally, what sort of deal are you, the buyer, making with the seller of the business? The structure of your deal needs to meet certain requirements.

Let’s examine each of these three broader categories in more detail

Can The Business Pay Back The Loan?

For the online business being acquired, the most important metric the SBA looks at is the business’s current earnings. The SBA wants to make sure you will be able to comfortably pay the loan with the business’s current earnings. Like many loans, this is determined by analyzing a debt to earnings ratio.

Currently, the SBA wants to see a debt to earnings ratio of 1.25:1 or better. In other words, for each dollar in loan payments, the business needs to make $1.25 in earnings. This ratio does change from time to time (it was 1.35:1 when we originally published this blog post in 2015).

Calculating the actual earnings of a business is, of course, crucial to getting to the right ratio. This process looks similar to what brokers use when we add back various expenses that may exist for the purposes of reducing a tax burden or for accounting purposes.

Keep in mind the SBA will want to make sure you are getting paid and can support your financial needs. Therefore, count on calculating your salary as a part of the debt to earnings ratio. If you have other sources of income (such as a secondary business), this can be included in the debt to earnings ratio which boosts your buying power.

3 Years Of Tax Returns Is Ideal, But You Might Qualify With Fewer Years

When you first explore an SBA loan for an acquisition, your banker will ask you for the last 3 years of US-based tax returns. In our experience at Quiet Light Brokerage, all of our deals have had at least 3 years of tax returns.

That said, the main concern of the SBA is whether the business can service the loan debt. If it is obvious it can be based on fewer years of tax returns, you’ll still be able to get approved.

This, of course, means the business being acquired has to be based in the U.S and have filed tax returns. Tax returns from other countries do not qualify.

Business Valuation

During the loan process, your SBA bank will hire an independent valuation company to value the business you want to acquire. While there are different ways to value a company, most independent valuation companies will use an earnings multiplier approach similar to what most brokerage firms use.

If your business valuation comes in lower than what you offered for the business, your bank will make their loan based on the valuation.

For example, if you offered $1,000,000 for a business, but the professional valuation comes in at just $900,000, the SBA will extend a note for $675,000 (75% of the $900,000).

Those of you who are quick at math may notice that I already said a buyer puts in 10%, and with the SBA giving 75% that leaves 15% left for the seller to finance on their own. I’ll explain deal structure later in this post (and why you, as a buyer, might want to do more than 10% at close).

What Does The Business Look Like Under Your Ownership?

While the business being acquired needs to meet certain debt to earnings ratios, you, as the buyer, have an impact on that ratio. Depending on your financial picture, you can make that ratio easier or more difficult to hit.

Your lending bank will examine a few key questions before agreeing to offer a loan:

- Your Finances – what is your financial picture? Is your debt to income ratio outside of what the SBA requires? What does your debt to income ratio look like if you acquire this business?

- Your Income – do you have enough money to support yourself and your family? If you acquire this business, will it need to pay your salary? If so, how do the debt to income ratios change?

- Your Credit Rating – it’s a loan, of course they will look at your credit rating. The higher the score, the better. Below 640 would be a problem.

- Your Equity Injection – I’ll look at down-payment requirements later, but you’ll need to have at least 10% of the purchase price. Be sure these funds are sitting in an account (any account – IRA, stock, savings, etc) at least 2 months prior to the closing date.

- Recent Debt – even if you qualify financially for a SBA loan, a bank may still turn down your loan if you recently took on a lot of other debt.

- Your Real Estate Assets – while many SBA loans are extended without a real estate security, some banks may nevertheless require it. SBA rules limit banks to only securing the loan against real estate, so your other assets are safe.

- Your Resume – if you are highly qualified and well suited for your acquisition, this will help you secure a loan.

While all of this might sound intimidating, you can easily run your personal financial situation by a lender to see if your situation will be an issue (much more on this later).

Every bank requires you fill out an personal financial statement which we include in our comprehensive SBA Starter Kit. Download your copy today.

SBA Deal Structures: Four Deal Structure Limitations

Since the SBA is guaranteeing the loan for you to buy a business, they have some requirements for both the buyer and the seller when it comes to the structure of your deal. For both the buyer and seller, most of these requirements are highly favorable.

The SBA Will Lend Up to 75-80% of The Purchase Price

For deals less than $500,000, the SBA will guarantee up to 80% of the purchase price of the acquisition. For deals more than $500,000, the SBA will guarantee up to 75% of the purchase price. [The SBA lends up to $5 million.]

The remainder of the purchase price is the responsibility of the buyer and seller. This is often made up of a combination of seller financing and cash from the buyer.

The Buyer Is Responsible For At Least 10%

For the part of the loan that the bank will not cover, a buyer and seller may negotiate how that part of the purchase price is covered.

From the SBA’s perspective, they require the buyer commit to a minimum of 10% of the purchase price. So, for an acquisition where the purchase price is $500,000, the SBA only requires the buyer to place $50,000 as a down-payment.

A buyer does not have to limit their down-payment to 10%, though. You may decide to put in 20%, 25%, or as much as you can afford.

Any amount not covered by the SBA or by your down-payment has to be covered by seller financing. Lenders tend to prefer deals where there is seller financing as they believe a seller will be more motivated to provide an orderly transition if they have a financial stake in the future performance of the company.

That said, many sellers are reluctant to agree to seller financing.

Seller Financing Is Put On a 2-Year Standby

With an SBA deal, any seller financing is put on a minimum 2-year standby. This means for the first 24 months after the acquisition, the seller does not receive any payments on their portion of the loan.

Of course, most sellers are extremely reluctant to agree to these terms.

Therefore, most buyers try to cover as much of the purchase price as possible which is not covered by the SBA loan. Since this usually amounts to no more than 20-25%, you are still receiving payback on your down-payment within the first year of your acquisition.

Deal Structure No-No’s: Earn-Outs, Employment Contracts, Consulting Agreements, and Partial Buyouts

SBA deal structures tend to be pretty simple to understand as they are made up of just three parts: the bank loan, the buyer injection, and the seller financing.

Some buyers and sellers may want to delve into more complex deal structures, but this should be done cautiously.

In an SBA deal, the seller is not allowed to be an owner, officer, or employee of the company after selling it. This rules out employment contracts or partial buy-outs.

In addition, while the SBA expects there to be a consulting agreement to help with transition services, consulting agreements with heavy minimum payouts or performance bonuses can have a negative impact on first year cash flows. As a result, these are also generally not allowed. Earn-outs are also not allowed for the same reason.

If you are using an SBA loan to acquire an online business, keep your deal structure as simple as possible.

For the bank, SBA loans are obviously guaranteed by the U.S. Government. For an online business acquisition, this is a very good thing as online businesses are usually “hard-asset poor” and difficult to collateralize for banks.

The SBA gives banks the needed security to extend loans on “goodwill”, but even with this security, banks will not extend loans haphazardly. If a bank has a high default rate, it can affect their ability to extend new SBA loans.

The SBA Will Take a First Lien Position On All Business Assets

In a SBA loan, the bank and the SBA will take a first lien position on all the business assets. What this means is if the business were to go into receivership, the SBA would have the right to liquidate and collect payments first from any assets being sold.

After business assets, the SBA may move onto personal real estate assets with at least 25% equity, then any business real estate. Many banks, however, will extend SBA loans without real estate security.

Finally, expect your lender to require Key Person Life Insurance. This policy protects the bank and the SBA in the event of your death. When applying for an SBA loan, get your life insurance screening done early as this can take a few weeks to process.

One piece of good news is that “other personal assets” outside of real estate are no longer allowed to be considered by the SBA for debt repayment purposes.

Coming soon: The SBA loan process

Source: Quiet Light Brokerage Blog